- Rounds up 13.6% in 2020. Most courses are budgeting up to a 10% increase over 2019. A significant variable is the timing for the opening of ballparks, restaurants, and other entertainment venues. Colorado Rockies are at 40% for opening day. Everything is optimistically thinking there will be high retention of those introduced to golf in 2020.

- Florida reporting (William Stine) decreased rounds in February – March 2021. In contrast, resorts like Bandon Dunes and Big Cedar Lodge are effectively sold out for the year. I tried to book a foursome for three nights staying on property at Bandon to celebrate crossing 3 million miles flown on United. They were booked until mid-November. The agent suggested I call back in January 2022 when rooms are first released for next year. The rates at Big Cedar Lodge are so high, you could, for less money, including your airfare play in England, Ireland, Scotland, or Wales. Unfortunately, the golf courses and hotels are NOT accepting reservations. The first time England may open up is June 24.

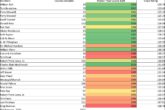

- The results of increased play are courses on the fringe of closing were able to continue in business. The current trend is for a reduction in the number of annual course closures. There was already a drop noted from 2019 to 2020 from 279.5 18-hole equivalents to 193.

- The demand for renovations at golf courses has picked up steam in the last six months. Members of the ASGCA, who had no or little work for the past 18 months, find themselves responding to multiple proposals in the 1st quarter of 2021.

- There is discussion emerging on northern courses on how to convert their facilities from seasonal to year-round functionality with the installation of simulators, conference room equipped with broadband Internet, activities for youth. Golf Club at Bear Dance, in Larkspur, Colorado, embracing the bold vision for the future clubhouse.

- Speculation increases how Troon will reorganize its acquisitions of Green Grass Partners, OB Sports, and Indigo Partners into a cohesive unit focused on the mid-tier daily fee and municipal markets. Too much overhead and duplicity of functions now exist within those three firms.

- Courses that had Season Passes in 2020 underperformed as they were heavily overused, crowding out rack rate customers. In January 2021, Disney announced it is discontinuing its annual pass program. A wise move for the golf industry to adopt.

- On a per-hour basis, the industry remains one of the most inexpensive forms of entertainment available, with green fees and a cart at $51. Golf courses would be wised to implement demand pricing though the hurdle remains the sophomoric nature of that software feature within existing POS/TTRS systems. At the same time, most nine-hole rates are at 60% of the 18 holes green fee. At Scott Lake in Michigan, Jeff Hoag prices his nine-hole leagues at 77% of the nine-hole rate. Little pushback was received so that he now uses 77% at the rate for all his nine-hole play.

- Volunteers at municipalities and daily fee courses9are becoming the forefront focus based on Palm Beach litigation. My understanding is that because a municipality is a “non-profit,” it can use volunteers compensating in free golf. Daily fee golf courses, as documented by several Florida IRS lawsuits, can’t. Daily fee owners offering Ambassador Programs for discounted season passes and allowing kids to pick the range for unlimited range balls for the week are on thin ice.

- USGA has a memo open for comment until March 26, 2021, that golfers can retain amateur status by receiving up to $750 in cash from tournament prizes at a golf course. A huge negative impact to be experienced by the merchandise sales of PGA Pros merchandise sales that is core to their earnings. PGA strongly opposes.

- F&B is usually a loss leader. The limited take-out memos through 2020 reduced losses from the reduction of staffing requirements of seasonal employees and the ability to limit menus to popular core items reducing the risk of spoilage.

- NextGen releases a millennial study that bodes well for the industry concerning club fitting and membership sales. The average age was 29.6, 93% male with household income consistent with the industry at large, i.e., $100,000 ish playing 33 rounds last year compared to the industry average of 18.6.

- Op36, a franchised model of teaching, is gaining market momentum. The introduction to golf is, first and foremost a social experience with friends that allows for “shot euphoria” on a few strokes during the round via a Scramble or Captain’s choice format. One’s score and competition are far down the list.

- The separation in the efficient management of golf widens as management companies are more adept at the adoption of technology and marketing while most municipalities remain burdened by politics, Golf Advisory Committees, excess fringe benefit system, and a protected work environment. One needs to look no further than the City of Sarasota for an example of wasteful and inefficient management. If a municipality has fringe benefits of over 40%, the chances of generating sufficient cash flow to fund capital expenses is unlikely.

- A generation has been skipped in the leadership of the industry. With many management companies and Associations now dominated by individuals in their late 50’s and early 60’s, the major golf publications, i.e., Golf Digest and Golf Magazine, are now led by individuals in the late 20’s and mid 30’s (Hoyt McGarrity, Max Adler, Hally Leadbetter, etc.). The generation of those who are in their 40’s and early 50’s appears to have been skipped. The core reason may be how the younger generation has embraced social media and technology.

Share